After last year’s strikes in South Africa, platinum has been very much out of the news in 2013.

Yet global demand has hit record levels in the face of dwindling supply. The price now sits below its cost of production, which points to further supply shortages. And funding for exploration has all but dried up.

The case for platinum looks compelling.

So is it time to buy?

There’s record demand for platinum

Demand for platinum has never been higher. According to Johnson Matthey, a record of 8.4 million ounces is needed this year.

Just over three million ounces of that is needed by the car industry for catalytic converters. Another 2.75 million is used in jewellery (the Chinese can’t get enough of it, apparently).

About 1.8 million ounces comes from use in other industries. And another 765,000 from investment – particularly the new South African platinum ETF.

In fact, demand has been steadily growing since 2009. Yet the platinum price has been steadily falling since mid-2011, when it flirted briefly with the $2,000 mark.

Platinum’s all-time high came in 2008 at around $2,300. It’s $1,385 today. Its high for this year was $1,740 an ounce, in February. Its low: $1,300 in July.

You’d think perhaps that there has been an increase in supply – but there hasn’t. World platinum mine supply was fairly constant from 2007 to 2011, ranging between 5.9 million and 6.6 million ounces. But in 2012, that fell to 5.7 million and it hasn’t rebounded.

Something like 75% of global platinum supply comes from South Africa, where production has been falling since 2011. In 2012, around 750,000 ounces were estimated to be lost to strikes, stoppages and shaft closures.

Estimates for the cash cost of extracting platinum range from about $1,400 to $1,700 an ounce. When you add the cost of building the mine (mines tend to be very deep), and compound deficits over time, platinum mining – at $1,380 – becomes a very expensive loss-making exercise.

A mine can only lose money for so long before it gets shut down. At least four have closed this year already. As Chris Griffith of Anglo American Platinum says, the industry is moving from “volume to value”. In other words, only higher-grade (and so more profitable) rock is being mined. This all points to further supply falls in the future.

Meanwhile, although labour relations are in better shape than in 2012, they are still, as Griffith says, “some way from being normalised”. In short, everything about South African platinum production looks fragile to me.

The other main producers are Russia, where production has fallen from 835,000 ounces in 2011 to 780,000 in 2012, and Zimbabwe, whose production rose from 230,000 ounces in 2009 to 400,000 in 2012.

Do you want to invest in Russia, Zimbabwe or South Africa, in a business that is, for the most part, loss-making? It’s hardly a story to get speculators slavering. Meanwhile, the performance of North America’s largest producer, Stillwater, over the past few years has been – shall we say – patchy.

One area of platinum production does get me excited – recycling. An old catalytic converter is far richer in platinum than any rock Mother Nature has given us. But the growth in recycling is still not enough to meet demand.

The demand-supply deficit will grow, says Johnson Matthey, to 605,000 ounces in 2013. At some point the above-ground stock will run out – and the platinum price will no doubt rocket.

But when?

What’s been holding back the platinum price?

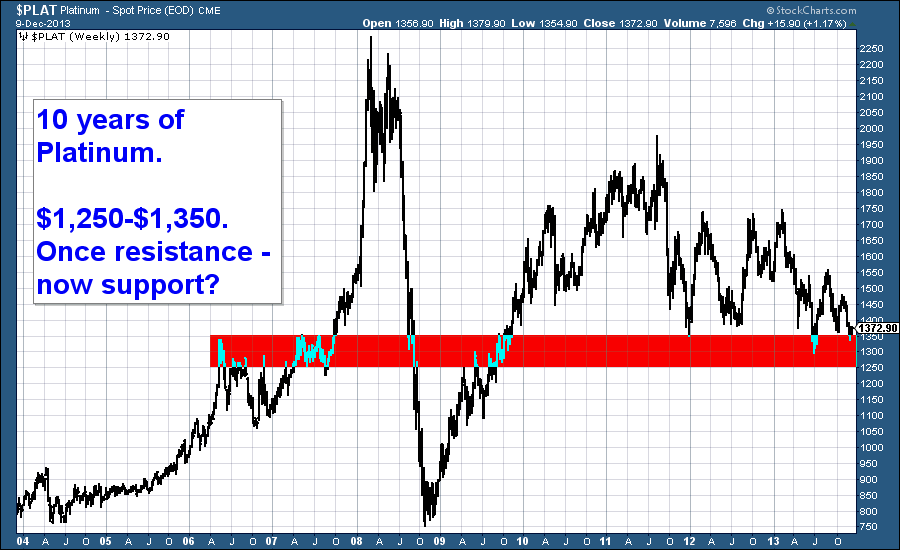

Below we see the platinum price since 2004. I have drawn a red band across the $1,250-$1,350 price area which was resistance in 2006-7 on the way up, and has provided some support on the way down.

Price-wise it has been a fairly significant inflection area for platinum.

Source: StockCharts.com

On a risk-reward basis, there might be a legitimate trade here to buy platinum with a stop just below that red band.

The ratio of gold to platinum is also low by historic standards – it’s almost 1:1 just now (ie platinum costs about the same as gold). It’s not unusual for platinum to cost twice as much as gold. On that basis, it also looks inexpensive.

So why has the price been falling in the face of such bullish fundamentals?

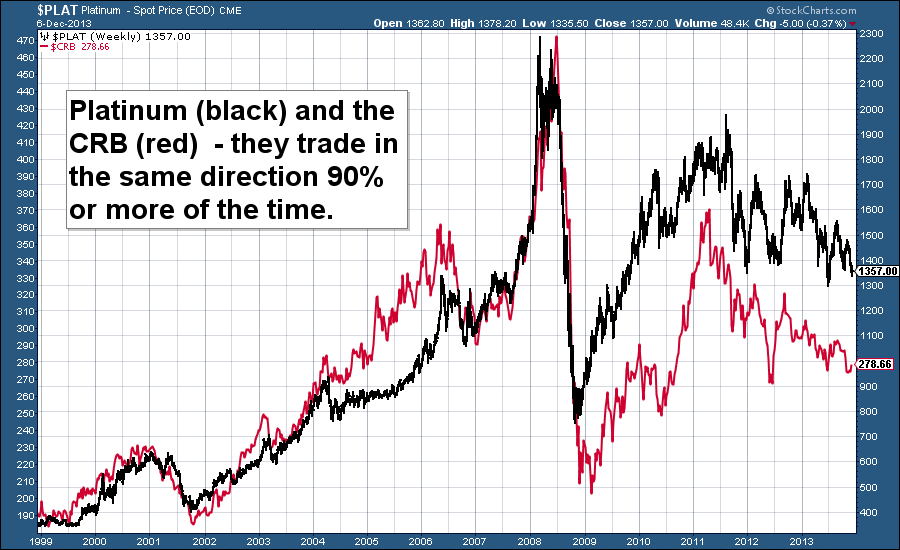

Here’s a 15-year chart that shows platinum in black, and commodities as measured by the CRB index (so that includes grains, softs, metals and energy) in red. You’ll notice that the two trade in the same direction almost all of the time.

Source: StockCharts.com

Of course, there are periods where one outperforms the other. But for the most part, they’re dancing the same dance. The CRB is about 75% weighted to energy, grains, meats and softs – things that have nothing to do with platinum. Yet, where it goes, so goes platinum.

So we have this Catch 22: commodities are in a bear market; they are trending down, and nobody knows quite when this will end. On the other hand, there is quite clearly a set-up for a supply squeeze and higher prices.

And platinum is not alone. The same set-up can be found in lead, zinc – perhaps even silver. Sooner or later these things are going to fly. And the companies that produce them – if they can survive this mining bear market – will too.

The question is when? I’m guessing sooner rather than later. I’m bullish on oil. Too many essential metals are trading below their cost of production, with supply squeezes dead ahead. I say we see a good rally in commodities starting early next year. Today’s dogs are tomorrow’s winners and all that.

Platinum’s time will come again. And I don’t believe that time is far away. If you’re interested in investing, there are various physical-metal backed exchange-traded funds available.

• Life After The State by Dominic Frisby is available at Amazon. An audiobook version is available here.

• Follow @dominicfrisby on Twitter.

Category: Market updates