Whatever your opinion on climate change, its increasing presence in political discourse is set to continue. The consequences of this – how governments decide to interfere in the economy in the name of climate change – is tricky to predict, and as a result, tricky for the market to price.

Whoever can figure out how the government will interfere ahead of the market, is going to make an awful lot of money. On Friday we explored how central bankers (led largely by our own Mark Carney) are flirting with the idea of turning their printing presses in the direction of green energy projects. This is something I reckon could make a fortune for whoever can invest in said projects ahead of the free money.

Today, I’d like to examine a different way the authorities will distort the economy in the name of fighting climate change. This has actually been in the works for a few years – but the deadline is swiftly approaching.

In an issue of Exponential Investor earlier this year, my colleague Harry Hamburg quoted a statistic that is as extraordinary as it is incendiary:

Back in 2009, confidential data was released showing one container ship produces as much pollution as 50 million cars.

To put that into perspective, there are only 31.3 million cars in the entire of the UK.

It’s estimated there are around 1.4 billion cars in the world. So 28 cargo ships produce as much pollution as all the cars in the world.

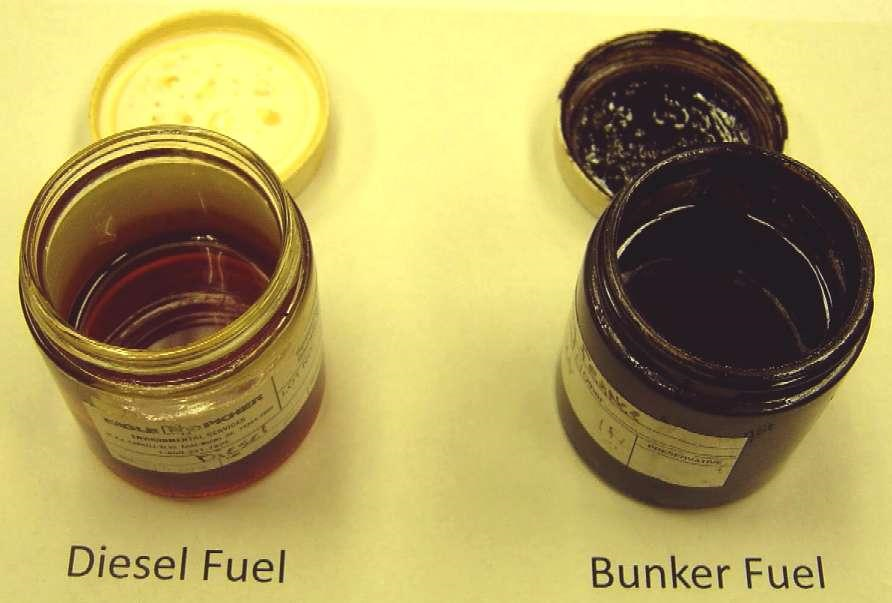

Container ships, once they’re out of port and have entered international waters (where they’re free from strict emissions standards), burn some of the filthiest fuel you can imagine. This is known as bunker fuel, or heavy fuel oil (HFO), and it contains 3,500 times as much sulphur as road diesel.

Source: Bluebird Marine Systems

Source: Bluebird Marine Systems

It’s the use of this fuel that (by 2009 standards at least) a single container vessel can produce far more pollution than all the cars in the UK.

But that’s all going to change next year. In 2016, the UN’s shipping authority, the International Maritime Organisation (IMO), announced a global cap on sulphur emissions which would be enforced by 2020. This has the capacity to have significant ripple effects throughout the global economy, not to mention in financial markets, as shipping is the main route through which anything is transported around the globe.

Increasing the cost of this basic input to global trade will have numerous consequences, in more ways than can be anticipated.

According to BP, the cheapest way for ships to comply with the rules is to keep using the bunker fuel, but buy exhaust “scrubbers”, which reduce the level of sulphur emitted. However, those scrubbers require vast amounts of water, which gets polluted in the process – and is illegal to dump back into the ocean.

So where will all this water go, and be stored? Somewhere on board? This would reduce space on container vessels, and increase prices to those using them, who would then make price increases of their own to their customers, and so on.

Maersk, the largest container shipper in the world, has indicated it will begin using marine gas oil (MGO) to comply with the sulphur cap, and this is looking like the more popular option. But MGO is much more expensive than bunker fuel, again increasing shipping costs, and puts significant stress on the refineries that will face a deluge of MGO orders, and a lack of bunker fuel orders.

The technology required for refineries to produce MGO comes with a billion-dollar price tag, and a 5-7 year period to develop, and doesn’t seem to be ready.

From HIS Markit:

The two industries are vastly unprepared. Neither has made the necessary investments for compliance, which means that the 2020 implementation date will result in a scramble…

Shippers will face significant compliance costs by having to upgrade equipment or switch to more expensive fuels. Refiners will experience significant price impacts as they shift production to deliver more lower-sulfur fuels to the market and, at the same time, find a market for the higher-sulfur fuels they produce. Refineries, like ships, do not turn on a dime, so it takes significant investment and market demand to retool a refinery to deliver new supply.

There doesn’t seem to be a way in which the shipping industry does not face increased costs in the future due to political actions driven by climate change. These increased costs (which some speculate will bankrupt some shippers) will have a larger impact than on the stock prices of the dozens of listed shipping companies around the world, however.

If those costs are then passed on to all of the industries which use shipping (there’s everything in those containers from base materials to t-shirts to iPhones) then everyone could end up paying more… for almost everything that isn’t domestically sourced.

High energy prices choke economic growth. And while high energy prices can be an organic result of supply and demand in the market, they can also, like in this case, be forced higher by decree. And in a globalised world which relies and uses more transport and more energy than ever before, the negative effect of higher energy prices is magnified.

This is against a backdrop of a world more indebted than ever before that requires economic growth to escape those debts. Should the authorities choke that growth off by increasing energy prices in their crusade against climate change (the IMO sulphur cap being just one example), they may find themselves confronting an entirely different enemy – deflation.

Boaz Shoshan

Editor, Capital & Conflict

Category: Market updates