Remember, we are actively competing with nations who openly cut interest rates so that now many are actually getting paid when they pay off their loan, known as negative interest. Who heard of such a thing?

Give me some of that.

Give me some of that money, I want some of that money.

Our Federal Reserve doesn’t let us do it!

I don’t say— Thank you, thank you.

The smart people are clapping.

Only the smart people are clapping.

– Donald Trump, giving a speech to the economic club of New York earlier this month

Spring 2014. Coming up to almost six short years ago.

While Obama was pushing a $1 billion deployment of troops to Europe, ISIS had just declared their establishment of a caliphate.

The Ebola outbreak in West Africa was beginning to occupy the headlines.

Maria Sharapova was still winning grand slams, Interstellar hadn’t been released yet, the Scottish independence debate was in full swing, and…

… there was zero negative yielding debt in the world.

Then June came along. And Super Mario at the ECB thought it was time to get the party started with some negative interest rates.

A bold move to be sure, but you don’t get the title “super” for nothing. Such prefixes must be earned.

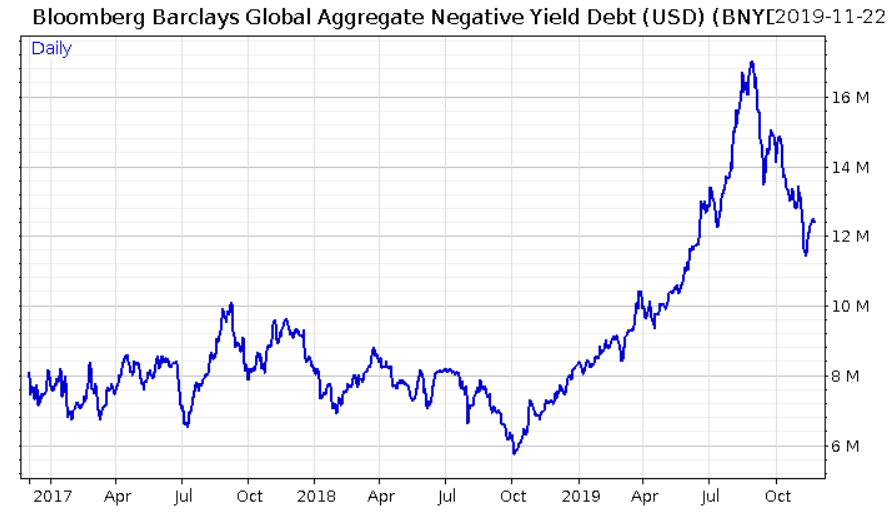

Fast forward five years, and there’s now over £9 trillion worth of negative yielding debt out there. Here’s lookin’ at you, Mario:

Outstanding negative yielding debt, in USD millions

Outstanding negative yielding debt, in USD millions

With so many investors paying £100.01+ for £100 in the future, it’s little wonder that Trump wants in on the game. Who wouldn’t?

Unless inflation comes back in a big way to the real economy and push interest rates meaningfully higher, we are strolling into a world where any enterprise with any hope of ever making any money can raise vast quantities of capital.

Dreams of future money

We’ve written often in this letter the strange and extreme lengths investors have gone in recent years to find interest, yield, or returns in general in a world where risk free interest rates are nigh-on impossible to find.

When interest rates go down, the value of potential future cash-flows goes up. You can see this simple relationship expressed in the stock and bond markets of the world, but they’re only half the story.

Those markets are public, in plain sight, and the prices of those assets are discovered by the market forces of buyers and sellers. What’s hidden is what goes on in the private markets.

Since 2006, some $5 trillion dollars has poured into “privates”: private equity, or PE. PE funds invested in companies that haven’t been listed on a stock exchange, but are prepared to sell stakes in the business.

The magic trick that can be played in private markets is that everybody can mark their own homework. The price of stock in these unlisted companies is not discovered by market forces, but instead by the small numbers of accountants involved in buying them.

Ever more investors are flocking to PE, with hedge, pension, and sovereign wealth funds racing to the trough. In fact, so much capital has flooded into the PE, that if companies which have raised money privately opt to go public, investors are already bored.

As Matt Levine wrote in Bloomberg recently, an Initial Public Offering, or IPO, has for many companies in effect become an FPO – a Final Public Offering, which is really just an exit strategy for the “privates” who invested first:

“Private markets are the new public markets,” I often say, meaning both that companies that once would have gone public can now stay private longer while still raising lots of money, and also that traditionally public-market investors are increasingly investing in private markets.

But that doesn’t mean that there are no more differentiations between types of companies or investors or funding rounds. It’s not that brand-new startups raise multibillion-dollar Series A rounds from Fidelity. Just like in the past, there still tends to be a discrete point where a company decides to raise a large funding round and open itself up to big public institutional investors. It’s just that in the past that point was the initial public offering, but now it’s the “FPO”: the Final Public Offering.

“The overall level of interest in doing investments ahead of IPOs is insane—it’s through the roof,” says Andrea Walne, a partner at Manhattan Venture Partners LLC, which focuses on this market. “People feel as though they can lock in the same value as the VCs they admire and respect.” Her business card reads “Tomorrow’s IPOs Today,” with a trademark symbol above the phrase…

Two points about this shift. One is that it should make IPOs a lot less fun. We talked about this dynamic in the Uber IPO: All the big investors who might want to buy Uber stock in an IPO had already bought Uber stock, so some of the thrill—and the demand—was gone…

The other point is that if this shift is permanent and growing, you should expect to see it sort of formalized at investment banks. Banks that put a lot of effort and creativity into pitching IPOs, and that compete fiercely for the fees and league-table credit involved, might start putting some of the same effort into pitching FPO advisory assignments. If FPOs are where the money is, you should expect them to be where the banks are too…

We’ll return to this topic tomorrow. You may be concerned that trillions of cash from pension and insurance funds has been poured into illiquid companies at crazy valuations, but don’t worry about it – the smart people are clapping.

All the best,

Boaz Shoshan

Editor, Capital & Conflict

Category: Market updates