It’s always difficult to predict the state of the economy. But at the moment, I don’t even know what state it’s currently in.

Unemployment around the world is impressively low. Monetary policy is pushing extraordinary amounts of stimulus. Growth and inflation are mediocre. Government deficits remain high.

So on the one hand, it’s taking vast amounts of stimulus to keep things moving. But things are moving fairly well.

The trouble is, we’re a long way into the global recovery. Depending on how you date things, it’s been around nine years. Europe’s sovereign debt crisis muddles the maths. The continent is recovering particularly badly. But it’s also on the largest amount of life support from its central bank.

Over in Japan, monetary policy is especially wild. The Bank of Japan bought 75% of government bonds issued in 2017 so far, and 40% of the total Japanese government debt outstanding. Without a hint of irony, the Governor proudly pointing out that “yields in Japan are stable”.

A Barclays trader reported that on Tuesday, not a single 10-year Japanese government bond traded hands. This is the biggest bond market in the world, with zero liquidity. It couldn’t be more fragile. And yet it couldn’t be more stable thanks to the BoJ.

But it’s not just Japanese central bankers that are on a buying spree. The Swiss central bank is a major shareholder in various American tech stocks, and possibly many other shares around the world without disclosing it. The ECB is running out of German bonds to buy inside its Capital Key rules.

It’s madness.

But what happens if you throw a recession into the mix?

A downturn before the recovery

Recessions are part of the business cycle. They come along eventually. Usually every seven or so years, making the nine-year recovery concerning in places like the US.

What if a recession struck now? What if one of the world’s major economies experiences a downturn?

Governments are deep in deficit, with debt approaching dangerous levels. A drop in GDP and tax revenue, and more borrowing, could bring on the return of sovereign debt crises.

Central bank interest rates remain too low to provide much stimulus by being reduced. QE hasn’t even ended yet. But it is of course infinite in theory. Except in the Eurozone, where rules limit how much the ECB can buy.

It seems a recession will be extremely difficult to fight off if it strikes now. Not that one can or should fight off a recession, but that’s what governments and economists believe they should do. So they’ll try.

But is there really such a risk? The American yield curve says yes.

Recession warning approaches

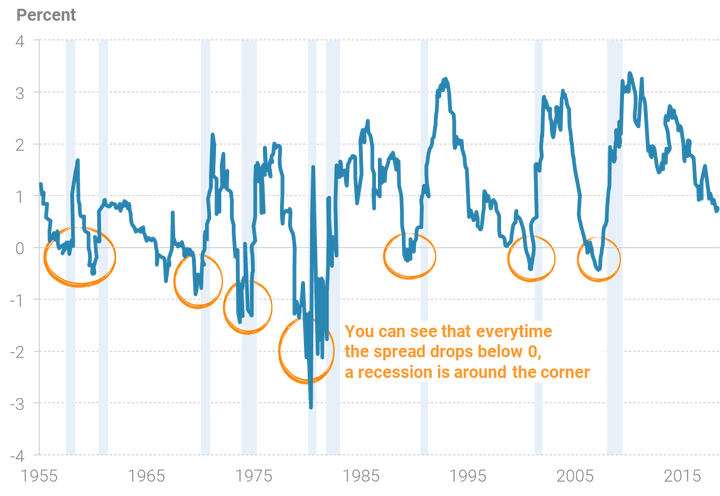

The yield curve is a line showing the yield of government bonds of different maturities. Usually, governments have to pay more to borrow for long periods of time for a variety of reasons.

But sometimes, the yield curve inverts, meaning the borrowing cost is higher for short term borrowing. When this happens in the US, it has been followed by a recession all but once since the 50s.

This chart shows another way of measuring the yield curve. When the line drops below zero, it means the yield curve has inverted. The concern right now is the dangerous downward trend.

Source: ETF Daily News

Source: ETF Daily News

For now, the yield curve has not inverted. It has been steadily flattening since the financial crisis ended – approaching 0. Such downtrends rarely escape a recession in the end.

GDP forecasts are tumbling too, largely in response to the yield curve’s predictive powers. In January the Atlanta Fed expected 5.4% GDP growth, but now just 1.9%.

The trouble is that the bonds which give you the yield curve are not trading in a free market. They’re subject to monetary policy. You might remember the name Operation Twist, which was an attempt to twist the yield curve using monetary policy.

Whether the yield curve’s ability to predict a recession holds true in a world of QE is an unknown.

Here in the UK, our economic growth isn’t far off from a recession to begin with. Economists are pointing to the uncertainty of Brexit as the reason why GDP growth will be below 1.5% in 2018.

“This is just a fact: Britain in 2018 and 2019 will have the lowest growth rates in the G-20 and this is due partly to the uncertainty linked to Brexit,” said OECD chief economist Alvaro Pereira. He’s inviting another embarrassing humiliation if his “facts” turn out to be wrong.

But if he gets it right thanks to an economic slowdown outside the UK, we’ll be in trouble too. And so will your portfolio.

Are stocks pricing the recession already?

Just like the yield curve, the stock market is supposed to be a good predictor. It tends to turn down before economists have realised we’re in a recession.

Perhaps the 10% correction in stocks in February was our warning.

But this recession could be different. If fiscal and monetary policy is a spent force, that means the support which stocks are used to these days could fail to show up.

If the economy manages to deliver a downturn in the face of deficit spending and monetary stimulus, where does that leave the stock market? Can central bankers keep markets afloat while the economy dips?

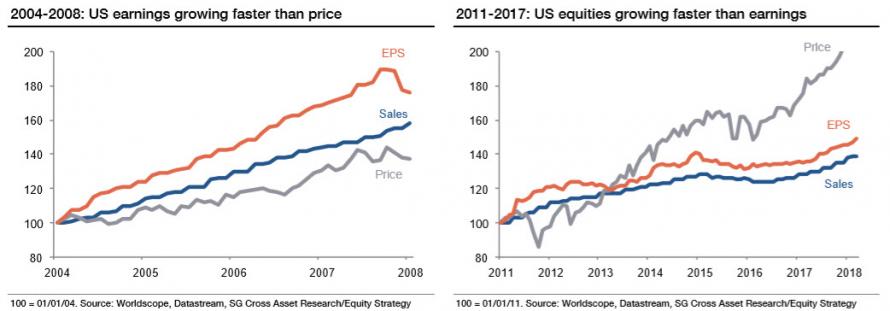

It’s particularly unlikely to work out well thanks to the position stocks are in now. This chart from Societe Generale shows why:

To the left, you have the American bull market that ended in 2007. To the right, the current bull market.

The message is that the current boom in the US stock market isn’t happening with the fundamentals to support it. Sales and profit (earnings per share) are not keeping pace with prices.

Strangely enough, Goldman Sachs uses the same sort of data to come to the opposite conclusion: “67% of the returns of this bull market were not driven by multiple expansion: a bull market where the preponderance of returns are from underlying earnings and dividends is unlikely to be in bubble territory.”

A third of gains are enough for me to worry!

Tim Price of London Investment Alert used the same arguments to warn of the 10% correction in stocks that began last month. But with markets recovering half of their losses, is the worst behind us?

Until next time,

Nick Hubble

Capital & Conflict

Related Articles:

- Time to buy a house in Ireland

- A change of heart in Brexit

- Your stock portfolio in ten years will be…

Category: Economics